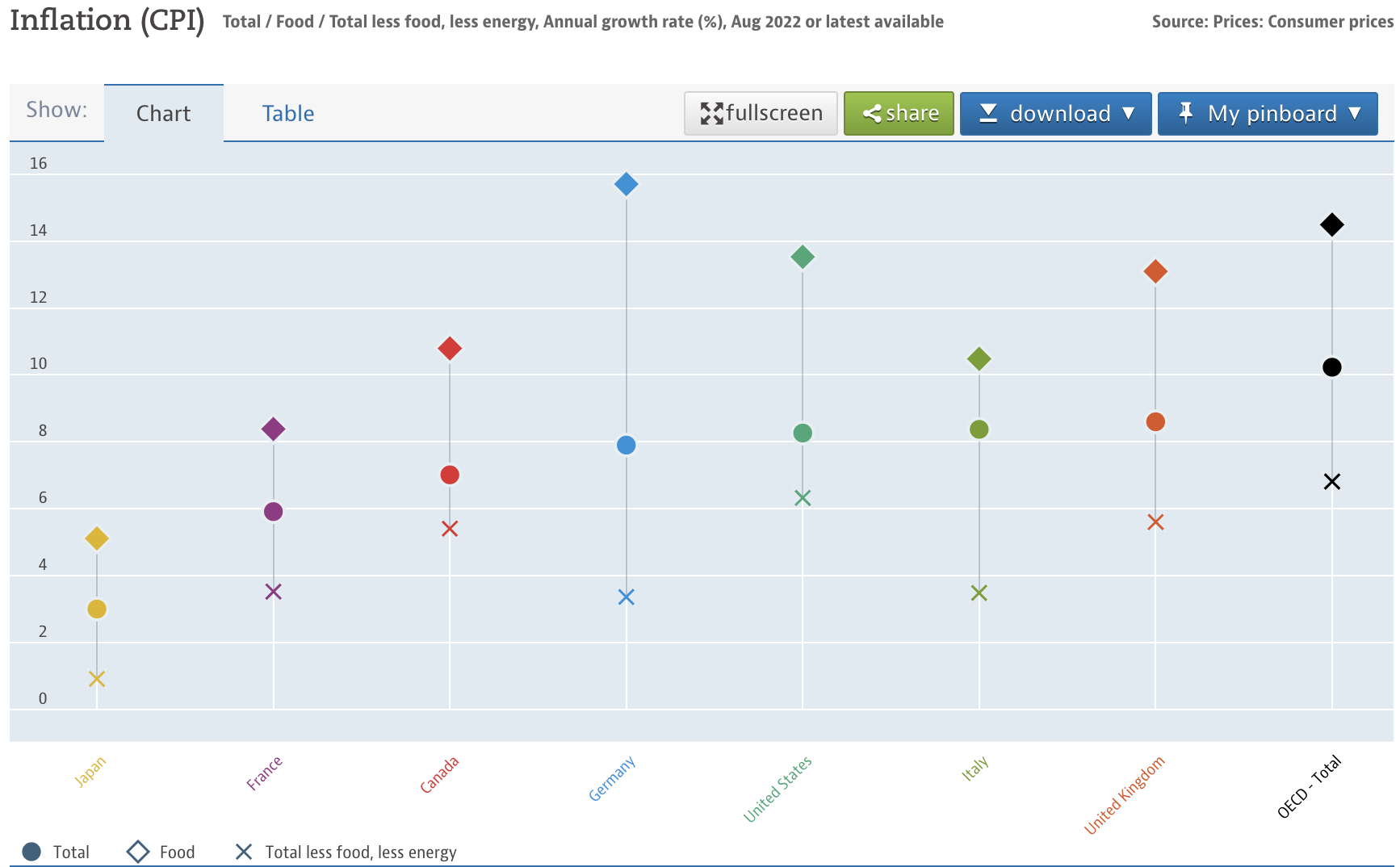

Let’s start with the big picture on interest rates. 90 central banks around the world have raised interest rates. This week, Indonesia, Norway, Philippines, Switzerland, Taiwan and the Bank of England all raised rates along with the Federal Reserve. Globally, the world is suffering from high bouts of inflation. The OECD chart below lists the damage to the largest economies and the OECD average.

To deal with inflation, the Fed raised rates yesterday by 75 basis points and indicated they expect to keep raising rates another 125 basis points by the end of 2022. If they follow through, this requires action to raise rates 75 basis points in November and 50 basis points in December.

The key question is why these levels?

To stop inflation, the Fed needs to end the monetary stimulus it created over the last 2 years to deal with the COVID shutdown. The Fed erred in 2021 when it believed inflation would be transitory despite rising levels and the new $1.9 trillion fiscal stimulus. This year’s delay gave inflation the ability to metastasize from goods to housing to services to rents to wages. The last 2 are sticky and problematic for the Fed. The supply chain issues were a symptom of the Fed’s over-stimulation/inaction and the Ukraine war sent all of this into a spiral the Fed now finds itself forced to act, and to act forcefully.

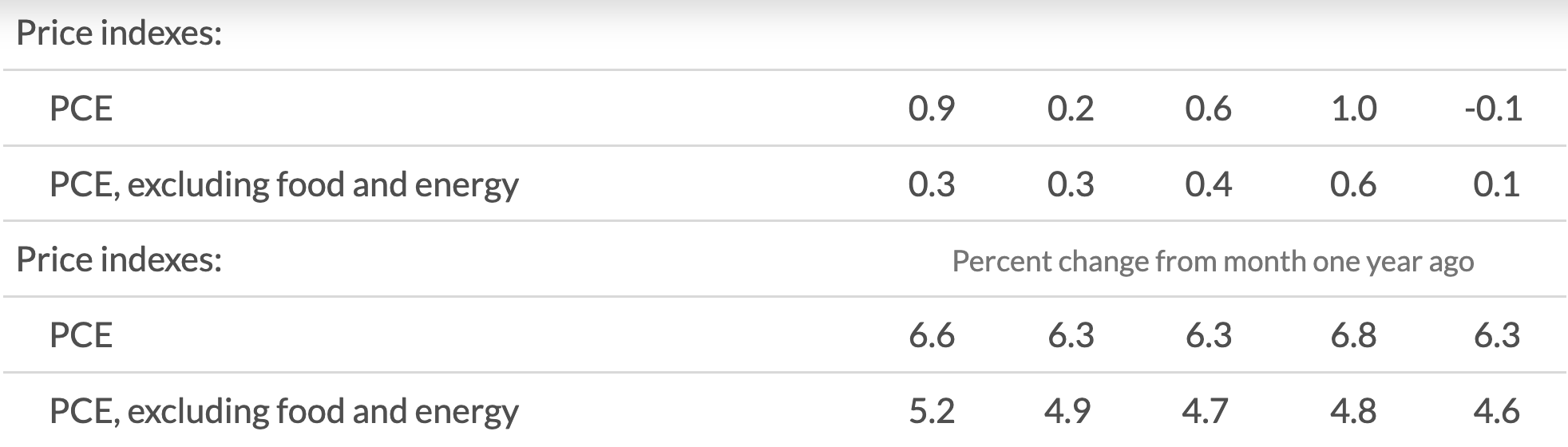

Back to the question of levels, the central bank is attempting to place interest rates above the rate of inflation. Yesterday, Chairman Jay Powell stated the Fed wants real interest rates above inflation across the entire yield curve. While the central bank monitors CPI for inflation, it uses another gauge to drive monetary policy actions. Core personal consumption expenditures is the preferred inflation guidepost. This gauge uses a basket of what consumers buy every month because it’s based on their spending. The table below shows the latest Bureau of Economic Analysis data.

Note the very last number on the right: 4.6%. This is what the Fed is targeting for Fed Funds. It’s why they want to raise rates to 4.5%.

Next Friday, we get updated data from the BEA on PCE. If core PCE drops, then we will see market expectations for future rate hikes drop and stock markets will likely rally. If core PCE rises, then we’ll see the opposite and stock markets will likely sell-off.

Sometimes our complex, chaotic financial world is really this simple.