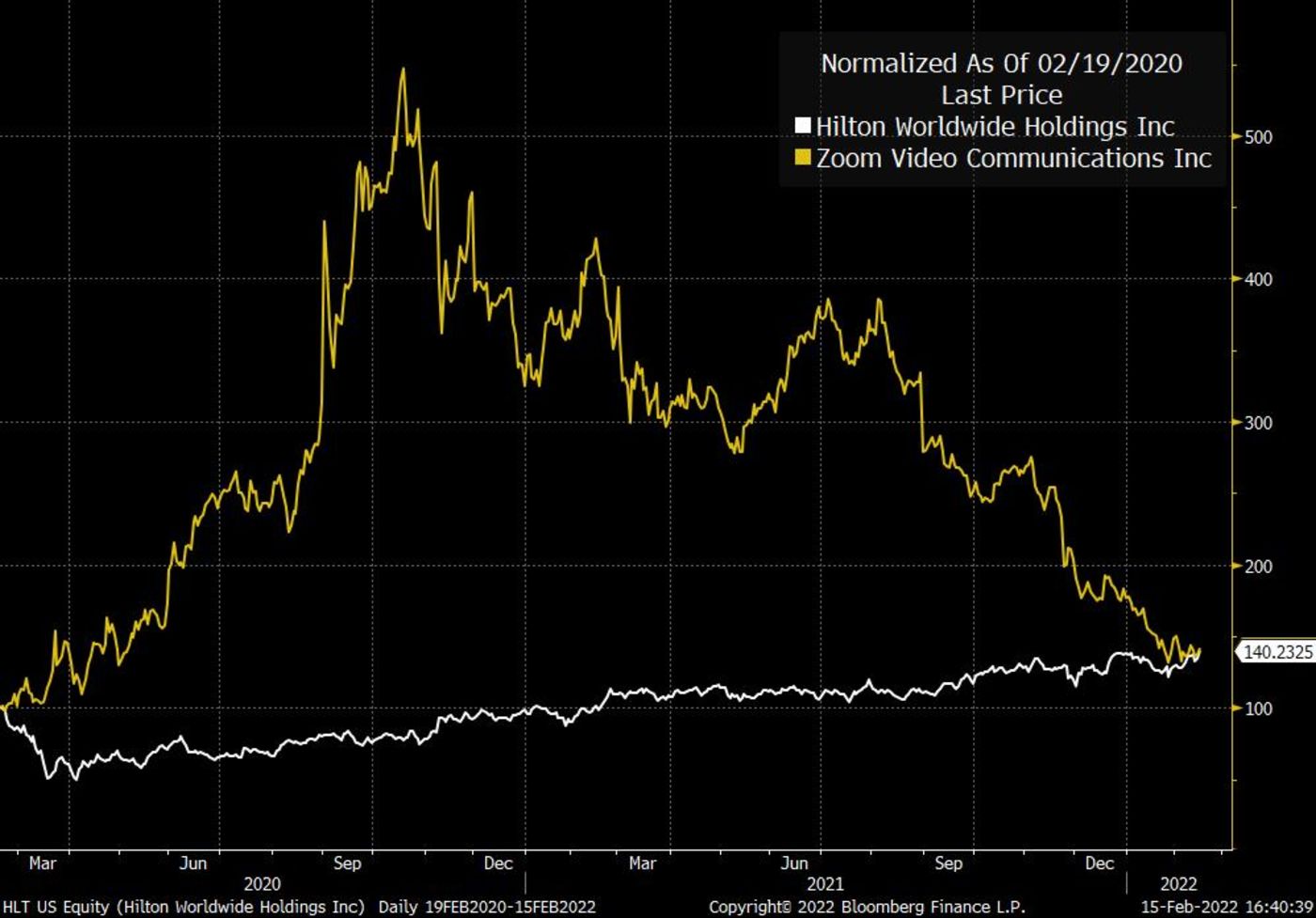

Ahead of the FOMC minutes, the markets have shrugged off the inflation news this week as the reduction in the Russia/Ukraine tensions have calmed fears. The shift from tech-above-all-else to revenge-of-the-non-nerds (reopening) has lifted parts of the market that had been beaten down due to COVID. The fact that Hilton (HLT) has nearly outperformed Zoom (Zoom) is emblematic of the recovery. (Bloomberg)

As companies report earnings and provide forward guidance, it’s easy to see the COVID mentality shift from pandemic to endemic to flu management. Moderna’s CEO Stephane Bancel said it is “reasonable” to assume that we may be approaching the final stages of the pandemic.

This statement is reflected in several recent events from the CDC softening its warning on cruise ships to schools across the country eliminating their mask mandates to the truckers strike in Canada. We’re not returning to “normal” but evolving into coping/managing the virus.

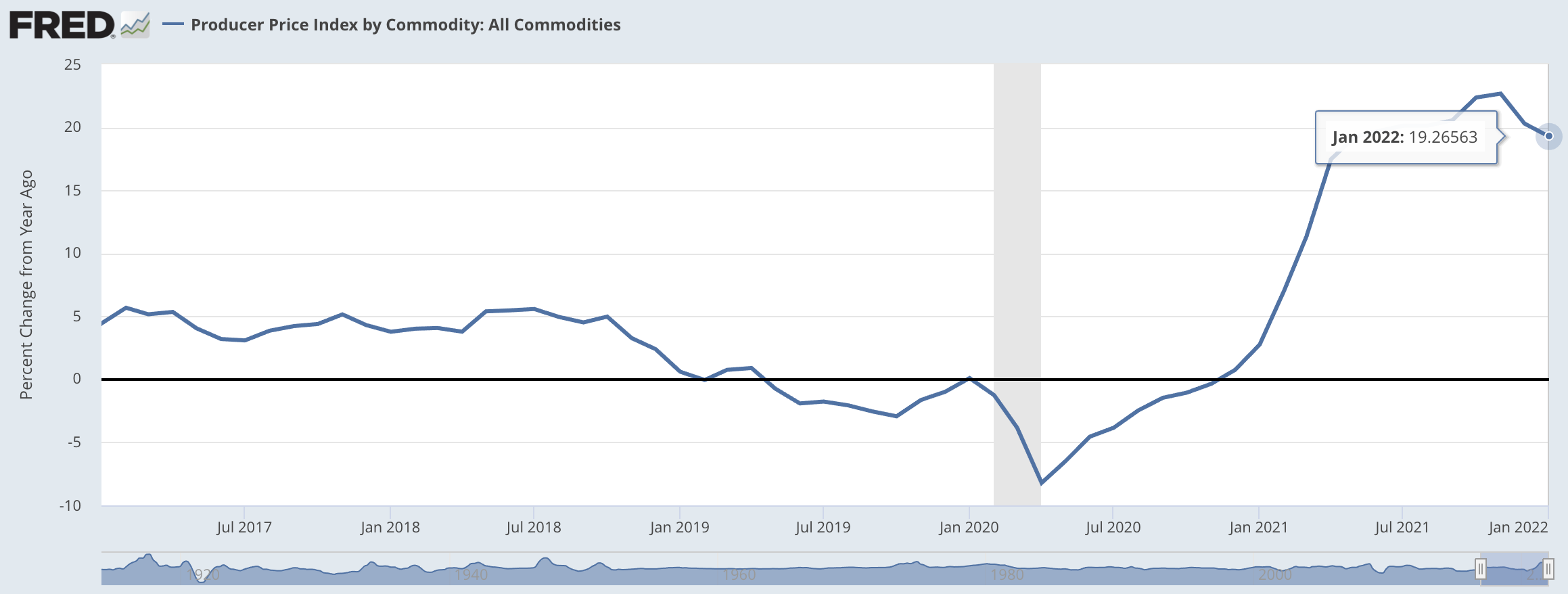

Yet, the largest remnant of the economic disruption remains with us. Inflation, generated via a shift in consumer spending from services to goods, remains virulent. CPI and PPI this week demonstrated how inflation remains embedded in the economy. With 10.9 million jobs open, labor pricing or wages will continue to put upward pressure in 2022.

This economic virus is not likely going to be contained simply by raising interest rates in the United States. Monetary policy doesn’t solve supply chain or labor supply issues with a few wand waving rate hikes. Nor does it solve the commodity demand/supply imbalance as under-investment in Capex will keep prices elevated for years. Want EVs? Better start increasing supply of copper, lithium, and cobalt or you’ll never reach your goals of Net Zero or even no ICE engines in CA by 2035. While you’re at it, the US needs oil as we’re still 1.5 million barrels below our output from 2019.

Given these problems, the bigger investor concern should be an exogenous event. The Russian/Ukraine situation was a fine example for energy, but how about China/Taiwan for chips? For food, how about a serious drought in the US Midwest. Or another rain bomb in Europe. Or a repeat of last summer’s heat in both the US West Coast and Europe? While Texas and Louisiana survived another potential Snowmeggdon recently, how about a series of hurricanes?

Yes, there are numerous examples of potential economic disruptions that could occur (asteroids!) and many more to list. The point is that we’re stretched on so many fronts we’ll likely have outsized impacts and potentially cascading effects across industries especially on prices.

Keep this in mind today as we get the FOMC minutes and the market’s reax to them. Prices may peak, but they won’t drop dramatically any time soon even with the economy slowing in Q1. People used to say lower for longer on interest rates. My take is to expect inflation to be higher for longer.