A Hint of Better Times Ahead

What’s astonishing about this data is how strong job creation was during a February cold snap that forced people to stay inside and a devastating storm which plunged Texas into the dark.

379,000 more workers found work in February, quite a surprise from the 225,000 expected.

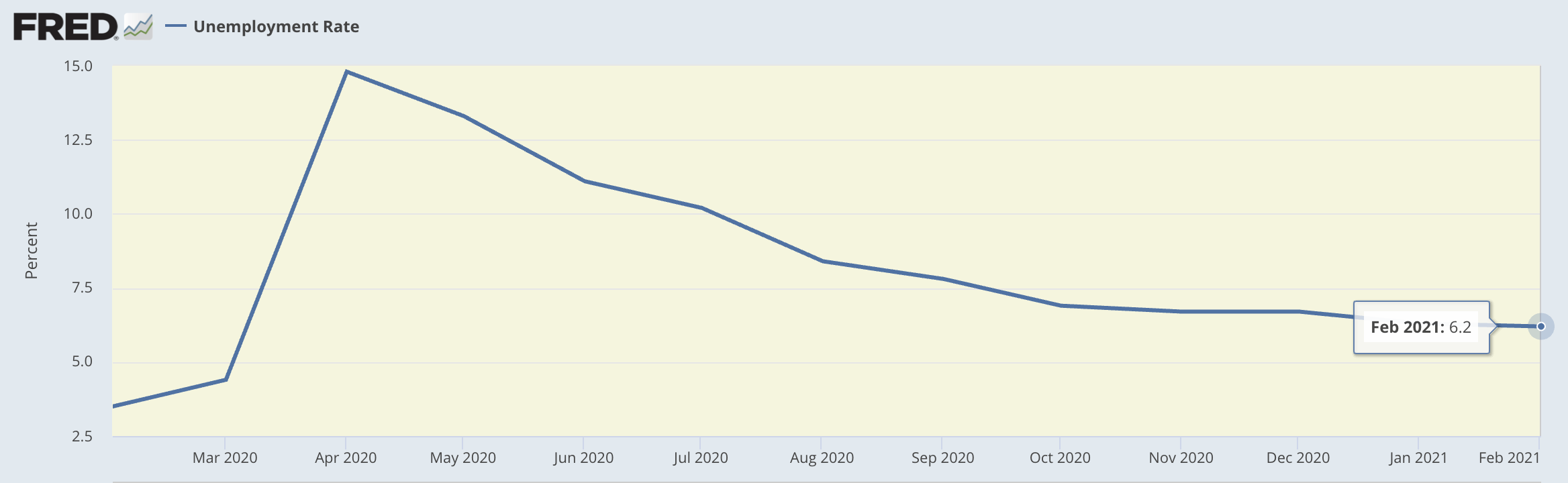

The unemployment rate was unchanged at 6.2% and the number of unemployed remained at 10.0 million, little changed from January.

If you’re wondering how this shakes out for the major worker groups/ethnicities, here’s the breakdown from the Bureau of Labor and Statics. The unemployment rate for Asians declined to 5.1 percent in February. The rates for adult men (6.0 percent), adult women (5.9 percent), teenagers (13.9 percent), Whites (5.6 percent), Blacks (9.9 percent), and Hispanics (8.5 percent) all showed little or no change.

What does this mean for the economy and markets?

For the economy, it shows the continuing negative COVID impact on leisure & hospitality plus transportation. These remain significantly below where they were prior to the shutdown/outbreak. Yet, the job growth in February showed positive job creation in both of these sectors. Leisure and hospitality had gains of 57k, and transportation/warehousing had gains of 25k.

This means the economic healing is starting in these worst hit areas. With 25% of the population inoculated, another 8% having antibodies and J&J’s 1-shot wonder delivering 20M doses by the end of March, the outlook for a rapid recovery in these areas looks bright.

And then there’s the whether-we-need-this-much-at-all-but-here-it-comes-anyway $1.9T stimulus plan. Yes, support those 10M unemployed from COVID. Yet, $350B to state and local governments is likely unnecessary given that many states are running surpluses. (See what your state is going to get here) Similar to this, the optics on sending $1,400 checks to people who have jobs seems misplaced at best.

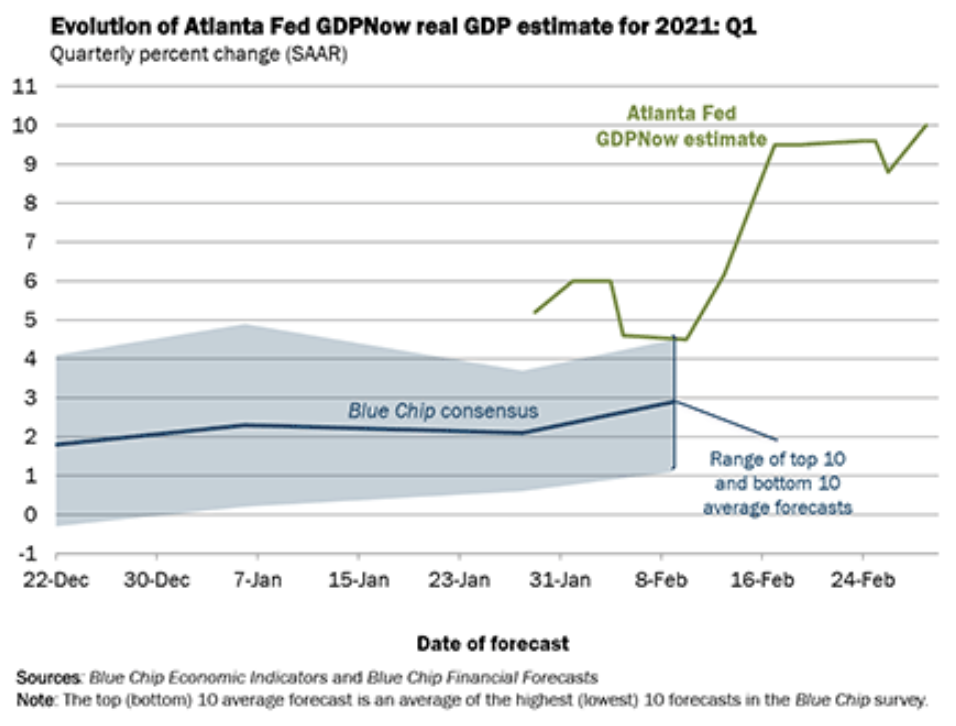

All of this wraps to rapid US economic growth, the “Future White Hot Coals Economy” I wrote about last month. The Federal Reserve of Atlanta’s GDPNOW is running at 10% for Q1 and the Federal Reserve of New York’s GDP Nowcast is at 8.68% for Q1.

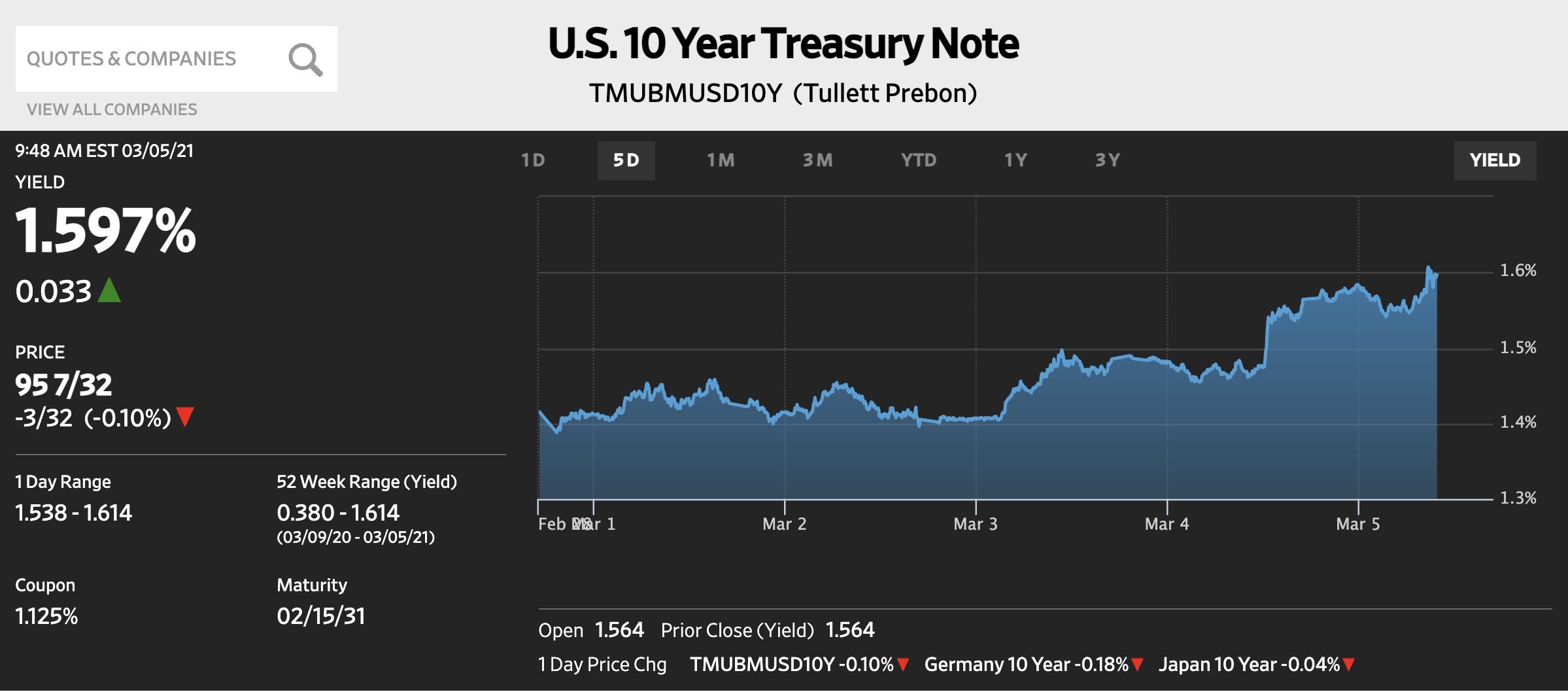

Is it any wonder US interest rates have shot up? The US 10yr note is up to 1.60% and the 30yr fixed rate mortgage is over 3.0%. I reckon these will continue to move higher as the vaccines are distributed and more workers are hired back.

This will put pressure on stocks, but not egregiously. The big problem will be speed and that’s what Powell/Fed are mainly worried about. Not the direction.

This means it’s likely the stock rotation will continue from outrageously priced tech stocks/bitcoin/alternatives to more mundane, undervalued value stocks.

Overall, unbelievably good job numbers to end winter and start spring. But steroid infused growth from the stimulus package will create building interest rate pressures on risky assets and bonds.